Most founders first hear about the YC deal through a tweet, YouTube video, or startup thread saying: “YC invests $500,000.”

It sounds simple until you actually open the documents and start seeing terms like SAFE, MFN, uncapped, post-money, and dilution everywhere. That’s usually when the whole thing starts feeling much more complicated than expected. But once you break the structure down properly, the logic behind the deal is actually pretty straightforward.

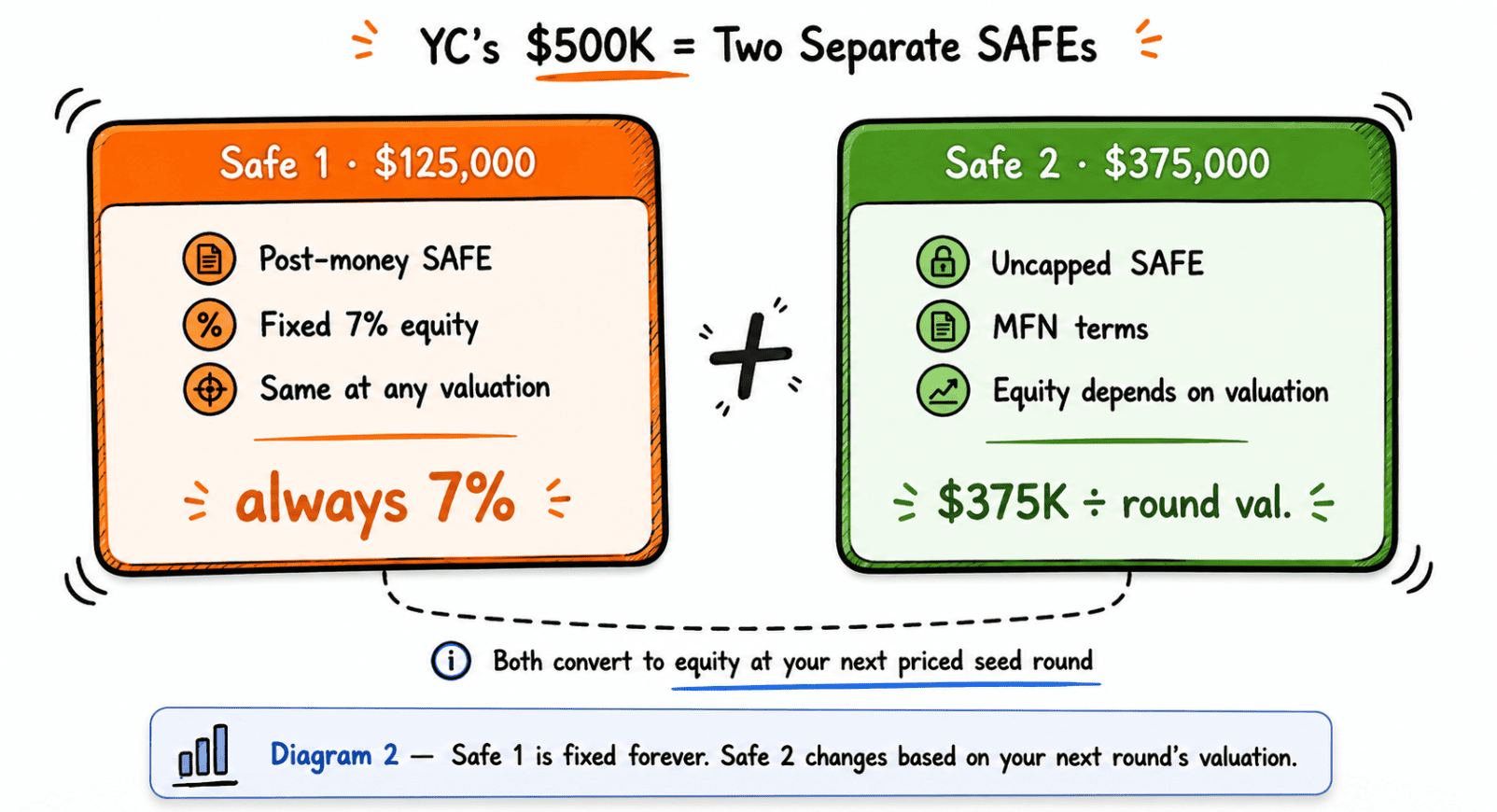

YC’s standard deal today is split into two separate investments: $125,000 for 7% equity, and another $375,000 invested through an uncapped MFN SAFE. Most of the confusion comes from the second part, not the first. Before understanding the structure itself, it helps to first understand valuation, because almost everything in startup fundraising comes back to that one concept.

Valuation is simply the agreed price of your company at a specific moment in time. Nobody bought your company. Nobody sold the company. It’s just a number founders and investors agree on so they can calculate ownership percentages. If your startup is worth $10 million and someone invests $1 million, they own 10% of the company. Higher valuation means you give away less ownership. Lower valuation means you give away more. That’s really the core idea behind startup dilution.

What is a SAFE

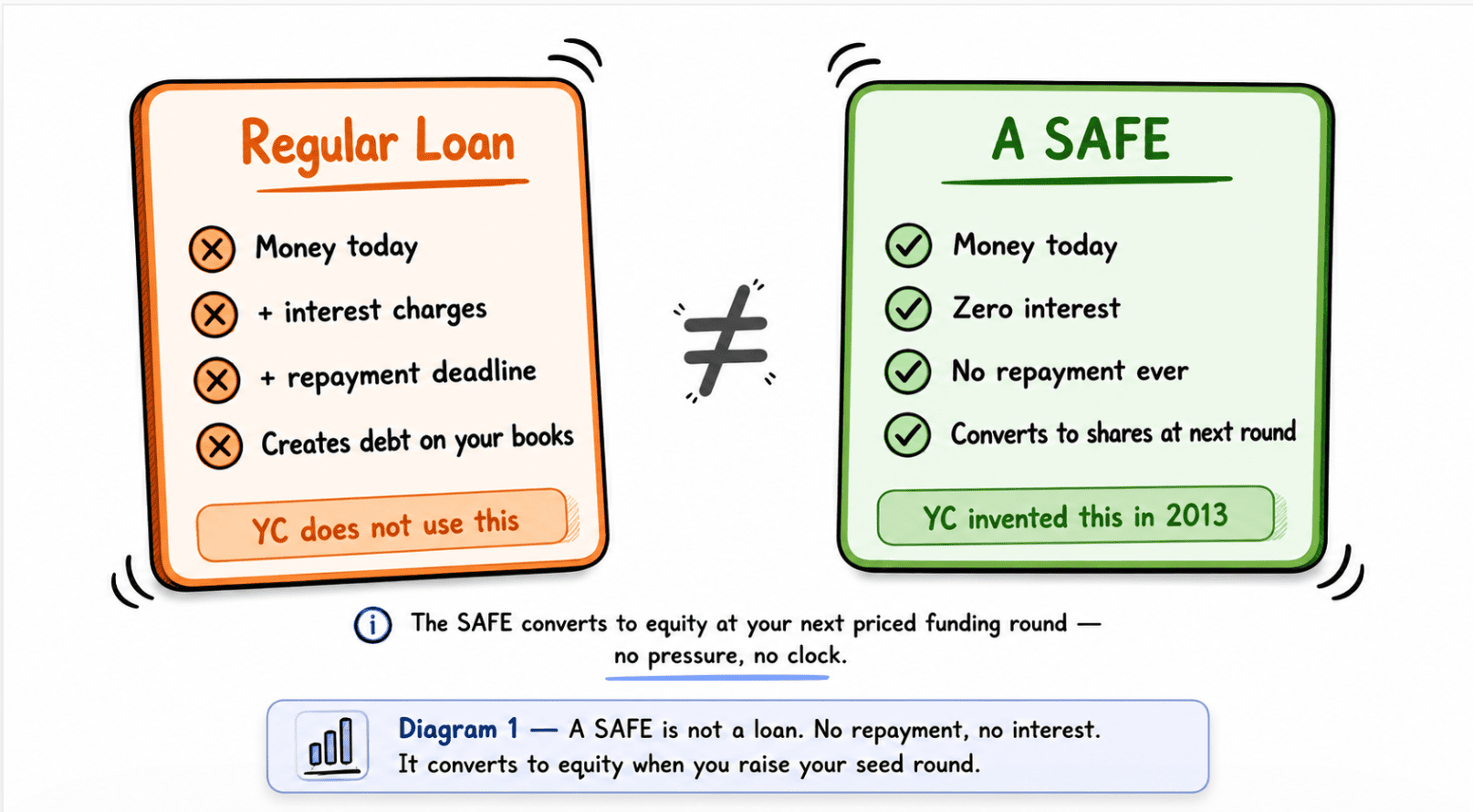

SAFE stands for Simple Agreement for Future Equity. YC created the SAFE in 2013, and today it has become the standard fundraising instrument for early-stage startups. The easiest way to think about a SAFE is that it’s not a loan. It’s simply an agreement that the investor will receive equity later.

There’s no interest, no repayment deadline, and no monthly payment. Founders take the money and use it to build the company. Later, when the startup raises a priced funding round where investors agree on an official company valuation, the SAFE converts into shares. Until that happens, the investor doesn’t technically own stock yet. They only own the right to receive shares later once the conversion happens.

Here’s a simple example. Priya’s startup raises money at a $5M valuation. An investor writes a $500K check, which means the investor owns 10% of the company. If Priya had raised at a $10M valuation instead, the exact same $500K would only buy 5%. The money stayed the same. The only thing that changed was the valuation.

Meet Priya and Marcus. They both got into YC.

Priya is building inventory software for independent restaurants. She has a working demo and two restaurants testing the product for free. Marcus is building an AI assistant for accountants. He already has 10 paying customers and $4K in monthly recurring revenue. Both got accepted into the same YC batch, and both received the exact same investment terms. There was no negotiation, no special treatment, and no custom structure based on traction.

That’s intentional. YC gives every startup the same deal because they want founders focused on building instead of wasting time comparing term sheets. The $500K investment is split into two separate SAFEs.

Safe 1: The $125K that locks in 7% forever

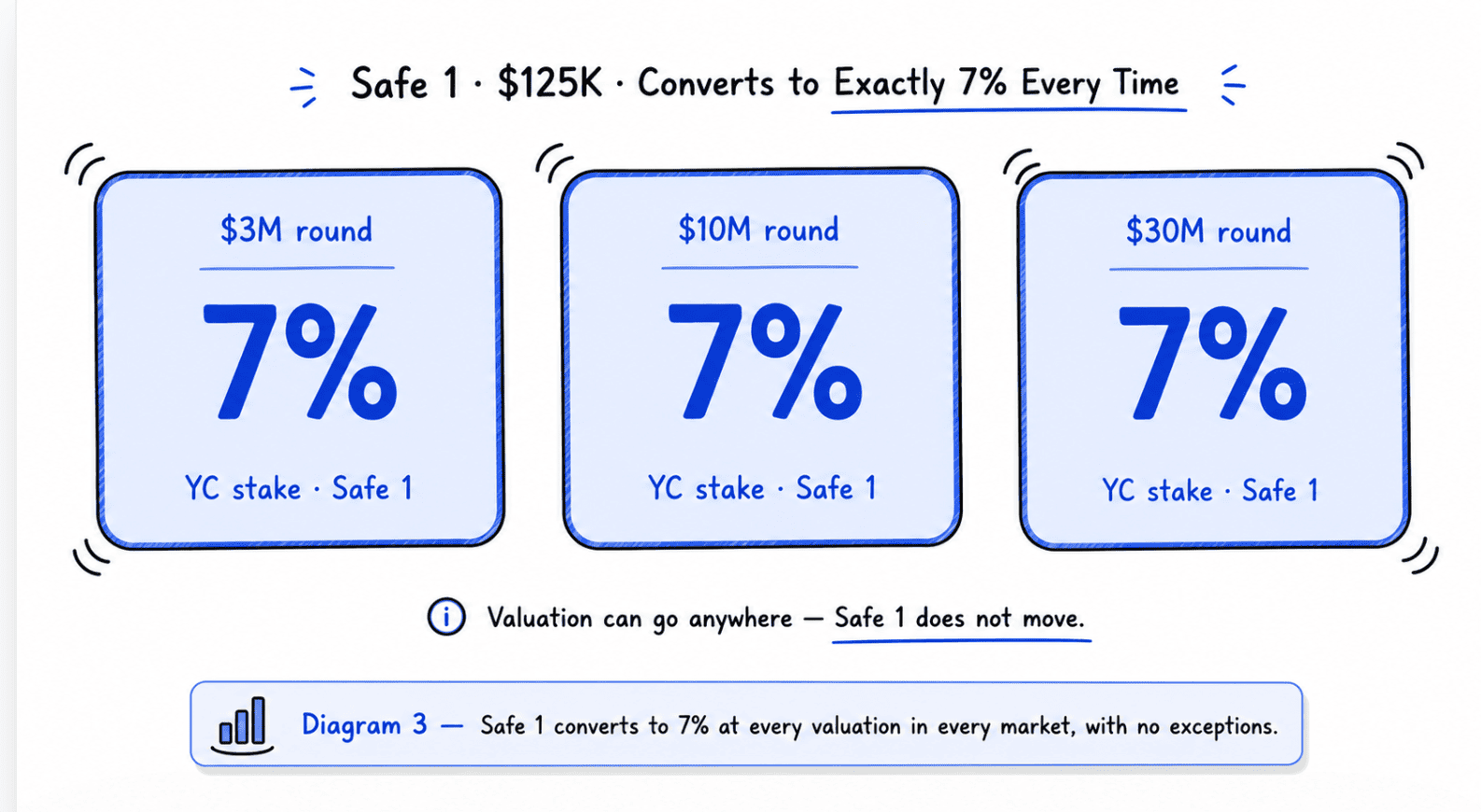

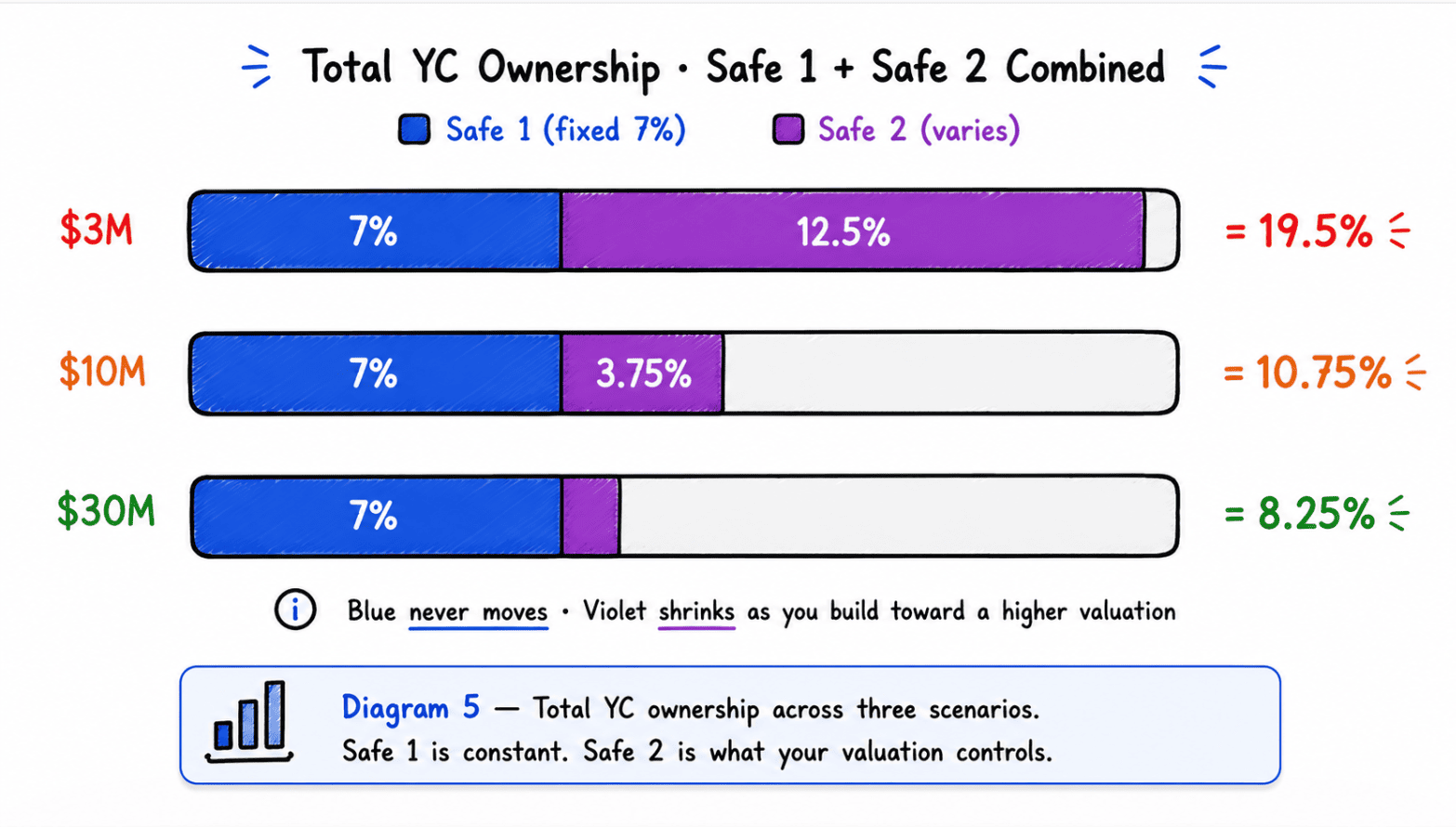

The first part of the deal is the predictable one. YC invests $125,000 through a post-money SAFE. “Post-money” sounds technical, but in practice it means something very simple: YC will own exactly 7% of your company when this SAFE converts, no matter what valuation you raise at later.

If Priya raises her next round at a $4 million valuation, YC still owns 7%. If Marcus raises at a $25 million valuation, YC still owns 7%. The number never changes. That’s why founders usually think of Safe 1 as the easy part of the YC deal, because from the moment you sign it, you already know exactly what you’re giving away.

And honestly, this structure makes sense for companies at the YC stage. Most startups entering YC are still extremely early. Sometimes it’s just a small team, an idea, and maybe an early product. YC is taking a meaningful risk at that point.

Safe 2: The $375K that changes with your valuation

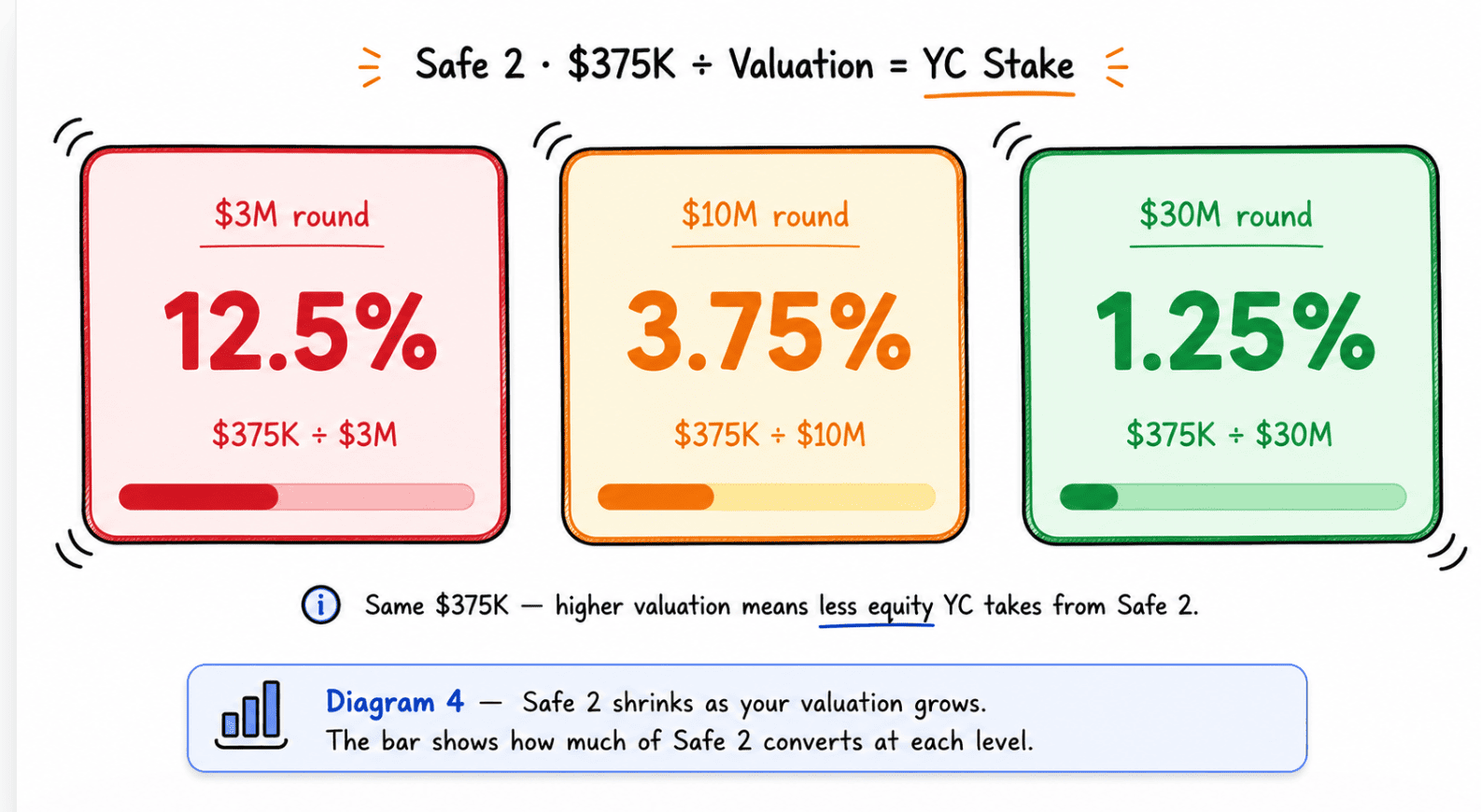

The second SAFE is where most founders get confused. YC invests another $375,000 through an uncapped SAFE with MFN terms. “Uncapped” simply means there’s no fixed valuation attached to this SAFE ahead of time. Instead, the SAFE waits until your next funding round and converts using whatever valuation your future investors agree on.

Because of that, the amount of ownership YC receives from this SAFE depends entirely on your future valuation. The math itself is actually very simple: ownership percentage = investment ÷ valuation.

Priya raises at a $3 million valuation, so YC’s $375K SAFE converts into 12.5% ownership. Marcus raises at a $30 million valuation, so the exact same SAFE converts into only 1.25%. Same investment amount. Completely different outcomes. The difference comes entirely from the valuation each founder was able to achieve before fundraising.

Now let’s talk about MFN. MFN stands for Most Favored Nation. The term sounds more intimidating than the actual concept. It basically means that if you later give another investor better SAFE terms, YC automatically gets those same better terms too. The clause exists to make sure YC doesn’t end up with worse terms than future investors.

The three scenarios, side by side

At this point, you can start seeing how both SAFEs work together. Safe 1 always stays fixed at 7%, while Safe 2 changes depending on the valuation of the next funding round. That means the more value founders create before fundraising, the more ownership they keep.

Why splitting it into two SAFEs is clever

Think about what would happen if YC invested the full $500K for only 7%. That would imply the startup is already worth more than $7 million before much has been built, which wouldn’t make sense for most companies entering YC.

Now imagine the opposite scenario where the entire $500K was uncapped. Founders who later raised at lower valuations could end up giving away a very large percentage of their company.

Splitting the investment into two SAFEs solves both problems. Safe 1 gives YC a predictable ownership stake for backing founders very early, while Safe 2 adjusts based on how much value the founders create afterward. If founders build something strong and raise at higher valuations later, Safe 2 becomes a much smaller percentage of the company. The structure mostly aligns incentives for both sides.

One thing founders sometimes underestimate is how expensive Safe 2 can become if they intentionally raise at a very low valuation just to close investors faster. Lower valuation means more dilution, and many founders don’t fully realize how much ownership they’re giving away until after the round closes.

The non-profit exception nobody talks about

If your company is structured as a non-profit, YC’s deal looks completely different. Instead of receiving $500K through SAFEs that convert into equity, nonprofits receive a $100K donation. There’s no equity, no ownership, and no conversion. YC gets nothing financially in return. (Source Wikipedia)

Very few people talk about this part of the program, but it’s actually one of the more interesting exceptions in YC’s model.

The whole thing in four sentences

YC gives startups $500K through two SAFEs that convert into equity later. Safe 1 is $125K for exactly 7% ownership, fixed forever regardless of valuation. Safe 2 is a $375K uncapped SAFE, so the ownership YC receives depends entirely on the valuation of the next funding round. The higher the valuation founders achieve later, the less ownership they give away from Safe 2.

Official YC Safe Agreement and Investment Terms

If you want to go deeper, YC publicly shares the exact investment structure and SAFE agreements used in the program. You can read the official details on the Y Combinator Deal Page and download the official SAFE documents from the YC SAFE Documents Page.

YC’s investment terms and program details can change over time. We tried to explain everything as accurately as possible, but small mistakes can happen, so always verify the latest information directly from the official Y Combinator website.

Adarsh is the founder and editor of Yeamt, where he breaks down AI, startups, funding, developer tools, and emerging technology into clear, practical explainers for founders, builders, and tech readers.